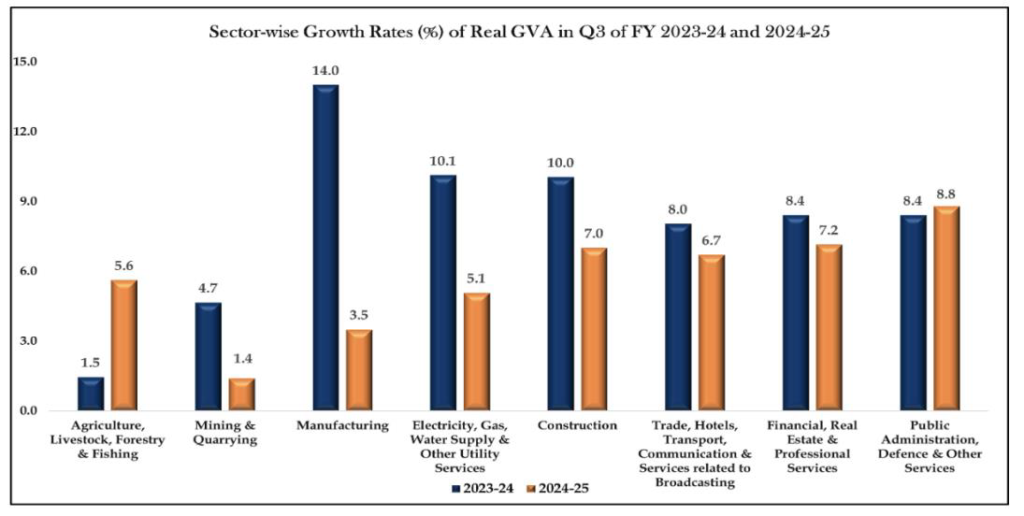

India’s economy picks up growth in Q3 2024-25. However, key sectors such as manufacturing, construction, and services face headwinds.

India’s economy grew in the July – September quarter of the current financial year (2024-25). According to the National Statistics Office (NSO) and the Ministry of Statistics, the gross domestic product (GDP) growth for Q3 2024-25 was recorded at 6.2%, well below the 9.5% recorded in the same quarter last fiscal year.

India’s unique economic pathway – but can it overcome the challenges?

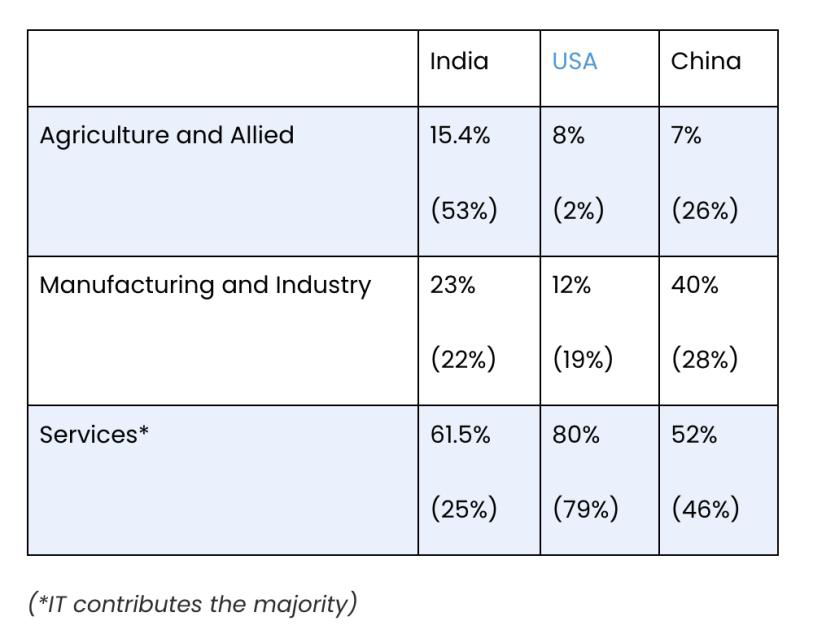

The economy’s sectoral composition indicates that India is neither following an American or Chinese economic model.

Figure 1 (numbers in brackets indicate employment percentages of the respective sectors)

Source: Invest India

The US economy thrives on its services sector. China enjoys its growth from the investment-led manufacturing industry.

India is attempting to draft its own unique economic pathway. Although agriculture contributes just over 15% to India’s GDP, it employs more than half of the country’s labour force. On the other hand, the services sector, which contributes almost two-thirds to the economy, only employs a quarter of the country’s workforce.

The latest data highlights this disparity. While the agriculture sector grew at an astounding rate of 5.6%, the manufacturing, construction, and all services sectors combined saw sluggish to moderate growth. With the bulk of the economy services – oriented, the slowdown in Q3 mirrors the decline in overall GDP growth for 2024-25.

Crunch the data further and other challenges also emerge

A deeper dive into the latest government data reveals more concerns on the horizon. In a conversation with ThePrint’s Deputy Editor, TCA Sharad Raghavan, Economist Radhika Pandey highlighted that:

- Overall investment remained stagnant at about 5% in Q3 2024-25, with private investment remaining “patchy” and state capex suffering contraction.

- Rural consumer consumption rose alongside agricultural growth, but urban consumption remained tight.

- Growth in per capita income (both in terms of real GDP/GVA and nominal GDP/GVA) slowed to 5% in 2024-25, down from 8% in 2023-24

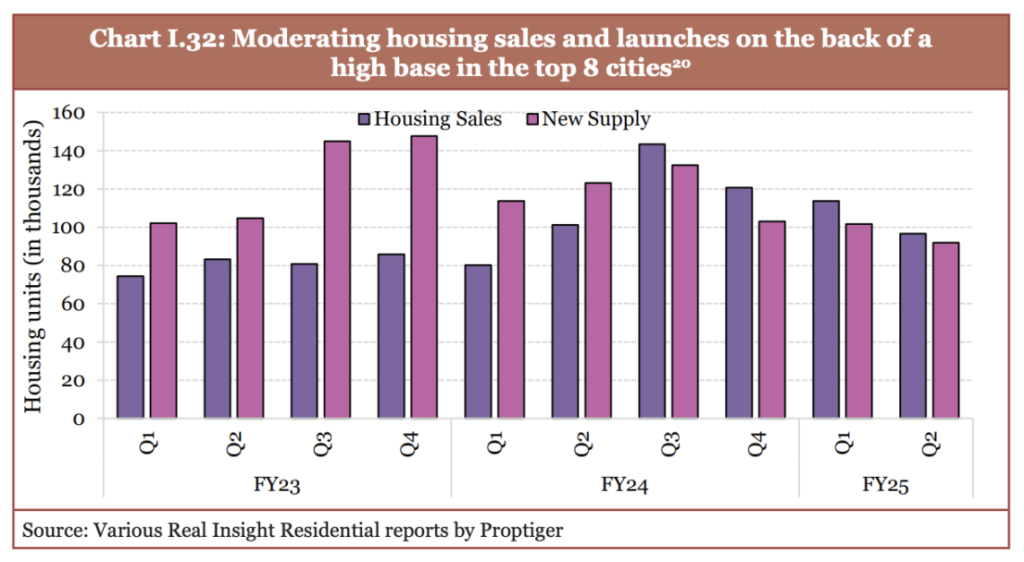

- As analysed by Pandey, “the real estate sector may have reached its peak.” The government’s 2024 Economic Survey indicates the same, with a consecutive-quarter decline in both house sales and new house builds.

Government acknowledges the challenges, but external risks loom

The 2024 Economic Survey highlights manufacturing suffering due to factors out of the government’s control – surplus monsoon and global supply chain constraints. It also recognises that future employment prospects for the youth lie in the services sector, with AI playing a critical role in upskilling the workforce.

However, external risks lie ahead for India:

- US President Donald Trump’s tariffs could lead to a global trade war – may impact India’s exports and certain sectors

- Strength of the USD against INR – may lead to higher import costs

- Stricter immigration policies in the OECD nations may reduce remittance inflows

- Ongoing global conflicts in Ukraine and Gaza add further uncertainty

Given the above, Pandey says the government’s expected Q4 2024-25 growth target of 7.6% remains a “challenging number” to achieve.